June 2023

We have written about this many times before but given the seriousness of our current emissions situations and the policies being introduced to address them, it stands to be repeated – there are nearly 300 million internal combustion engine vehicles (ICEVs) in the United States and 1.5 billion worldwide. Even as we transition to a greater reliance on battery electric (BEV) and fuel cell electric vehicles (FCEV), we have to explore opportunities to reduce emissions from the legacy fleet as well as the millions of ICEVs that will be sold over the coming years. For those passionate about electrification, this does not detract from your objective. Electrified vehicles are a key ingredient to meeting our emissions objectives, but they alone cannot accomplish this mission. Remember – the mission is not to transition to a new technology but to reduce and eliminate harmful emissions from the transportation sector. This is why the Transportation Energy Institute commissioned and will soon release its latest report, “Decarbonizing Combustion Vehicles – A Portfolio Approach to GHG Reductions.”

When we developed the scope of work that led to this project, we were quite mindful of the political dynamics that surround any discussions about transportation. The nation has bifurcated into the pro-EV and anti-EV camps and, unfortunately, some have assumed that if you are talking about combustion engines you must be anti-EV and, by association, anti-decarbonization. Nothing could be further from the truth and we wanted to ensure that this report is received by decision makers as another resource on which they can rely to accelerate the reduction of emissions from transportation. Below is a preview and summary of what this research found.

Fleet Turnover Takes a Long Time

First and foremost, we must accept that any transition to a new vehicle architecture will take decades. According to research by Oak Ridge National Laboratory, half of the light duty vehicles (LDVs) sold today will still be on the road in 16 years and 20% will still be on the road after 20-25 years. Even more, some will still be operational after 30 years. With regards to heavy duty vehicles, the life expectancy is much longer – half will still be running in 28 years and 20% will still be running after 34 years.

ICEVs Dominate the Current Market

We must also acknowledge the size and composition of the current vehicle market. Take the LDV segment for example. According to the U.S. Energy Information Administration (EIA), in 2022 there were around 257 million LDVs in operation in the U.S. Of these, more than 99% were equipped with an internal combustion engine that operated on liquid fuels. When we combine this data with that provided by Oak Ridge National Laboratory about vehicle longevity, we know there is a need to address the emissions from ICEVs. In addition, through May 2023, according to Wards Intelligence, American consumers had purchased 5.9 million vehicles with an ICE, representing 93% of LDVs sold during the first five months. If this trend continues, more than 14 million new ICEVs will enter American roads in 2023.

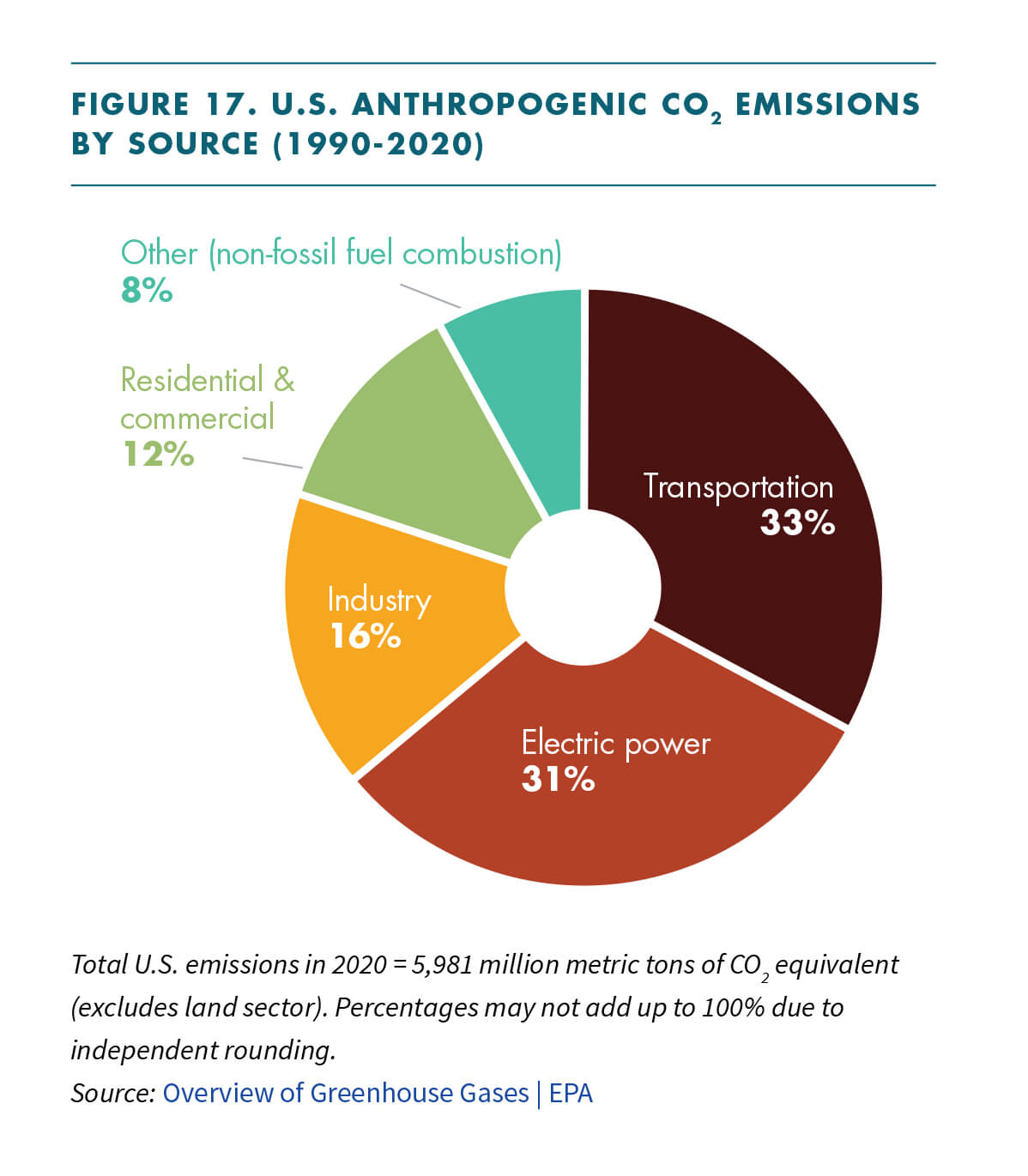

GHGs Stick Around a Long Time

According to the United Nations International Panel on Climate Change (IPCC), global human activity is responsible for 5% of CO2 emissions into the atmosphere, which is enough to offset the delicate balance of the naturally occurring carbon cycle. Of this, the United States accounts for 13.9% of emissions with transportation responsible for roughly one-third of that. It is important to recognize that these emissions remain in the atmosphere for up to and beyond 100 years. Consequently, if we are serious about reducing the concentration of harmful GHGs in the atmosphere, we need to start reducing emissions now from the current fleet even as we transition to new vehicle technologies.

Immediate Tools

Now that we have established the importance of addressing ICEV emissions, the next big question is how. It might be compelling to begin discussing new ICEV design and improvements in vehicle technology, but that does nothing to address the existing fleet. In January 2022, we published a report, “Life Cycle Analysis Comparison,” which demonstrated that 73% of life cycle GHG emissions from an ICEV come from the combustion of fuel. Consequently, improving the carbon intensity of the fuel being used by these vehicles is the primary pathway to achieving significant GHG reductions from the legacy and new ICEV fleet. The great thing about this fact is that we already have tools at our disposal that have been and can continue to achieve meaningful GHG reductions. By leveraging our existing biofuels industry, we have already made progress and can build upon that without having to retrofit any vehicles. In some instances, very minor and inexpensive after-market retrofits can take existing ICE further by allowing higher levels of low carbon use.

And moving beyond these traditional biofuel blends, our research found there are at least 24 biofuel sources that can be supplied and consumed by existing infrastructure and vehicles today that deliver a carbon intensity at or below that achieved with electric vehicles charged from today’s U.S. electricity mix (excluding coal). If we can find a way to capitalize on these options and get them to market, we can further reduce the GHG emissions from the ICEV fleet.

Other Progress Is Readily Available

Reducing the life cycle carbon intensity of the fuels we use in ICEVs should be a top priority. In addition to leveraging renewable fuels as demonstrated above, we can also make progress in reducing the carbon intensity (CI – gCO2e/MJ) of base petroleum and biofuels products. For example, the oil and refining industry can reduce the CI of gasoline and diesel fuel by substituting fossil natural gas used for energy generation with renewable natural gas or renewable sources of electricity; reducing or eliminating natural gas flaring in the oil fields; implementing carbon capture and storage where it could be most effective (this could reduce GHG emissions by 15% for gasoline production and 30% for diesel); and increasing energy efficiency throughout the refining process.

Meanwhile the biofuels industry can lower the CI of its products by utilizing best agronomic practices when growing required feedstocks; by using biodiesel and renewable diesel in farming equipment; by optimizing the production of wet distillers grains and solubles where possible to reduce energy required for the drying process; by using renewable energy to power their facilities; and by implementing carbon capture and storage (CCS) where it makes the most sense (this has the potential to reduce GHG emissions by up to 40%).

New and Emerging Low CI Opportunities

Beyond leveraging existing products and process improvements, there are other opportunities to deliver lower CI fuels for the ICEV fleet. All come with challenges that must be overcome, but the potential return on the effort could be substantial. Among the options analyzed in the report are:

- Increasing gasoline from 10% ethanol to 15% ethanol nation-wide and throughout the year.

- Using more biodiesel and renewable diesel in diesel equipped vehicles.

- Expanding production and use of renewable gasoline.

- Leveraging the CI benefits of renewable natural gas in natural gas vehicles.

- Diversifying feedstocks to support biofuel production by supporting the development of energy-specific crops on marginal lands.

- Using pyrolysis (thermal decomposition) of biomass to produce gasoline, diesel and propane.

- Applying a biomass to liquids process, using partial oxidation or gasification, to convert biomass or waste products into gasoline, diesel or propane.

- Developing a market for E-fuels (synthetic gasoline, diesel, propane or methane) by leveraging renewable energy to combine captured carbon dioxide with hydrogen to produce near zero carbon, drop-in ready fuels.

- Using hydrogen as a fuel for ICEVs.

Conclusion

Our transportation system is complex, dynamic, and long-standing. Solutions to reducing GHG emissions from the transportation sector must be equally dynamic and quickly implemented. There are a wide variety of options that can contribute to achieving the stated mission of reducing and eliminating harmful emissions. Our new report dives into these topics in greater detail, evaluates the pros and cons of different options, considers the scalability of biofuel options and compares the various options based upon their feasibility, carbon reduction potential, costs and difficulty. It is a resource to help guide discussions about the most effective and efficient ways to reduce GHG emissions from transportation.

If we combine a concerted effort to address emissions from ICEVs while we support the market expansion of new vehicle technologies, our ability to achieve the stated mission in a manner that preserves and protects access to affordable and reliable transportation energy will be greatly enhanced. This report is just one more tool to help us on our journey.