John Eichberger |

October 2025

Despite recent changes in policy priorities in Washington, DC, there remains consensus among global leaders to reduce carbon emissions from the transportation sector. To achieve global environmental objectives, however, we cannot wait for new technology vehicles to replace the 1.5 billion that are currently in operation around the world; we must find ways to reduce emissions from existing and new combustion engine vehicles. Fortunately, there are a variety of options that exist today or are in development that can contribute to a lower carbon intensity for liquid fuels used by vehicles that travel on the surface, in the water and in the air. One of the options in development that holds great promise is a product known as e-fuels, also referred to as synfuels or electro fuels. However, to contribute meaningfully to decarbonization across the transportation sector, e-fuels will have to become commercially available and be deployed at large scale.

In 2024, the Transportation Energy Institute (TEI) published a report on this topic, “E-fuels: Evaluating the Viability of Commercially Deploying E-fuels in Road Transport.” This study evaluated the technical readiness, environmental benefits, scalability, and economic competitiveness of e-fuels, focusing on their role in road transport and their interaction with other sectors. It found that the promise of e-fuels to contribute to a lower emissions transportation sector will rely heavily on government policy to enable the industry to scale and deliver fuels at a competitive cost, but that the societal benefits could justify the investment. Let’s start with explaining what e-fuels actually are.

What are e-fuels and why are they important?

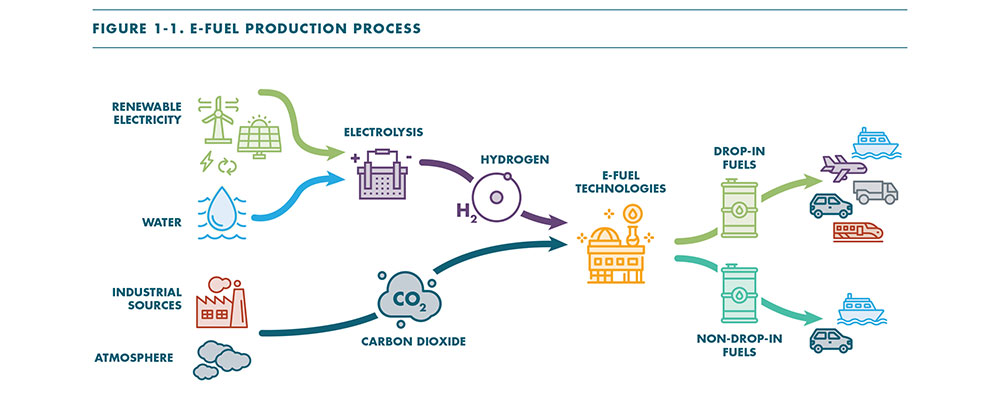

E-fuels are renewable fuels made from water, renewable electricity, and captured carbon dioxide (CO2) through chemical or biochemical processes that can be used in road, aviation, maritime, and rail sectors. The CO2 used in the process can be captured from the emissions of industrial facilities or potentially extracted directly from the air. Many of the e-fuels that can be produced are considered “drop-in” fuels, which are compatible with existing infrastructure and vehicles, while other products like alcohols might require vehicle or infrastructure modifications for high-blend use. The push to decarbonize transportation requires development of a variety of options that can lower the carbon intensity of fuels used in vehicles, which is why e-fuels seem to be an attractive option.

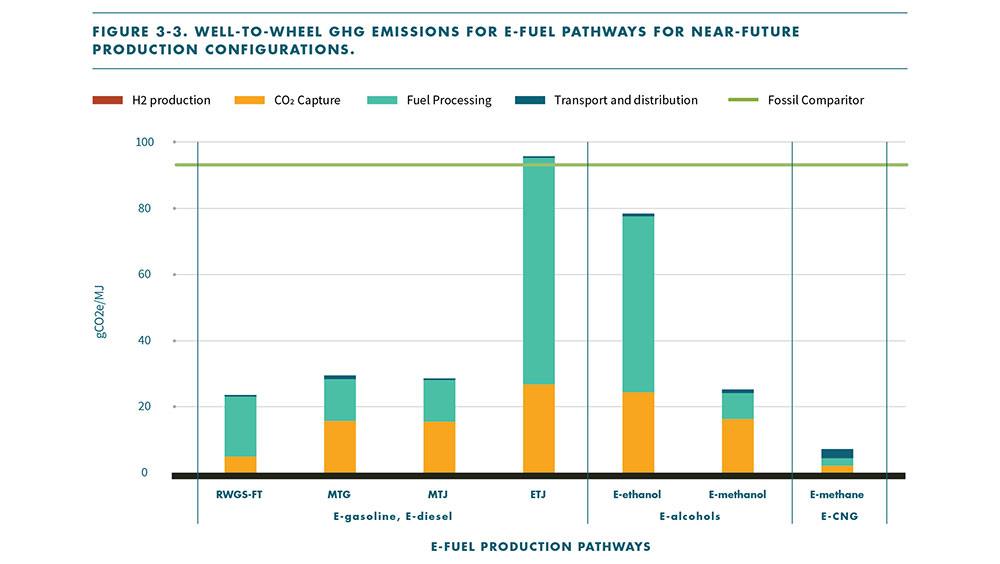

Depending on their production methodology and the source of feedstocks, e-fuels can achieve up to 75 – 99% reduction in life cycle greenhouse gas emissions (GHG) compared with fossil fuels. The figure below shows the lifecycle emission profile of early production facilities; however, it is projected that advanced facilities have the potential to drive GHG emissions for nearly all e-fuel products to near zero.

E-fuels represent an encouraging option in terms of marketability. Because many of these products are compatible with existing infrastructure and vehicles, bringing them to market will require little additional investment. In addition, the resources required to produce e-fuels are highly abundant, so scalability will not be feedstock-constrained. These are some of the reasons e-fuels have a great opportunity to play a significant role in the transportation sector. But there is a lot of work yet to be done.

How big can the e-fuels market become?

At this time, e-fuels are in the low stages of technological development with pilot and demonstration projects having only recently entered operation in the past two years. However, evaluating current and expected production capacity, e-fuels are projected to produce up to 27.5 billion gallons per year worldwide and 4.7 billion gallons in the U.S. by 2040. For U.S. production, the resources (renewable electricity and CO2) required to produce this volume is a very small percentage of the anticipated supply.

That said, 4.7 billion gallons represents just 1.5% of petroleum products consumed in the U.S. in 2024, and some may question the value of such a contribution. The low CI of e-fuels delivers a significant benefit to the market. By displacing 4.7 billion gallons of petroleum, e-fuels could reduce CO2 emissions in the U.S. by more than 50 million tons per year. In addition, because they are largely drop-in ready, they could play a significant role in reducing emissions from hard-to-abate sectors of the transportation market. But the question is not so much one of production feasibility, but affordability.

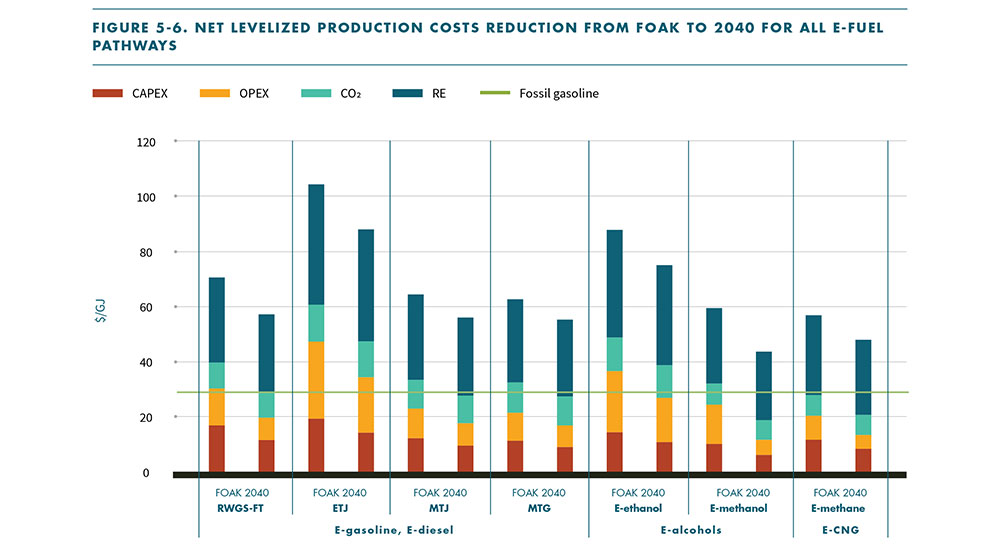

The analysis published by TEI estimated that e-fuels cost 2.5 – 4 times more than fossil fuels. This cost relationship puts e-fuels at a significant competitive disadvantage relative to traditional biofuels and direct vehicle electrification. The chart below shows the cost per gigajoule of power for a variety of e-fuels produced in “first of a kind” facilities (typically using early and less efficient technology) and in facilities expected to be in operation with advanced technologies in 2040. Each pathway is significantly more expensive than the benchmark cost of producing fossil gasoline. Yet, while some may immediately dismiss the potential because of this assessment, it is important to look at the full range of possibilities.

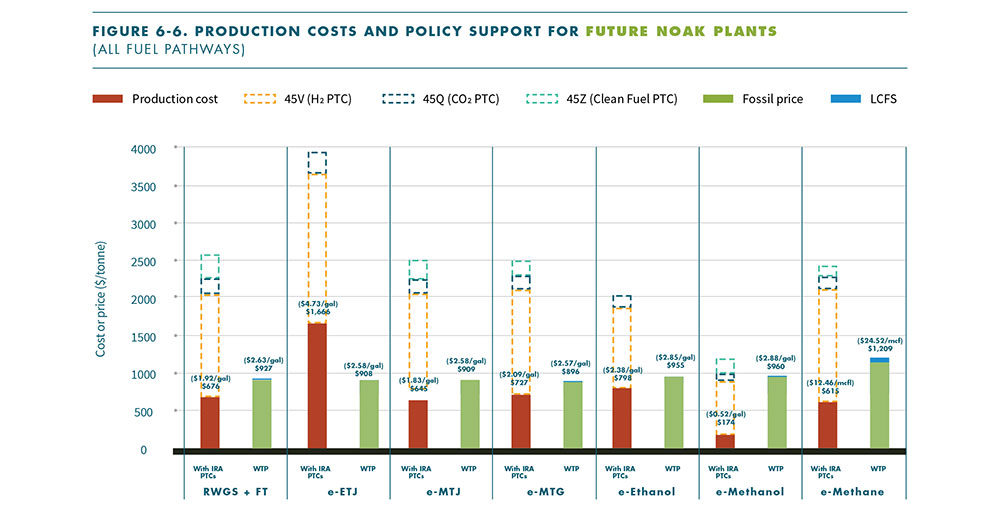

When this study was prepared in 2024, there were a variety of U.S. policies that could contribute to lowering the market cost of e-fuels if they were to remain on the books throughout the development of a market for the products. When these policies are combined and applied to each pathway, the result is a much more competitive outlook. The following chart shows the impact of these policies on facilities expected to be in operation in 2040 (a.k.a., “nth of a kind” plants). The production costs in this chart are compared with an expected “willingness to pay” (WTP) threshold. As can be seen, with the application of policy incentives, the cost of several e-fuels pathways can drop below the WTP threshold.

Conclusion

The case for e-fuels remains tenuous, but the underlying market facts still support further evaluation and development. We are confident that the motivation to reduce carbon emissions will not go away and we are convinced that internal combustion engine vehicles will remain in operation for decades, necessitating a low carbon fuel solution. The potential contribution to this objective represented by e-fuels is clear, but the challenges of scalability and cost reduction are significant. However, the drop-in nature of many e-fuels will obviate the need for significant investments in new infrastructure and new vehicles, which would lower the overall cost to society of bringing e-fuels to market. Regardless, it is most likely going to require collaborative industry-government strategy to achieve market viability for these products, but the ultimate potential benefits from such an effort could just inspire such collaboration.

For more insights into e-fuels, visit transportatioenergy.org to download the report or listen to TEI’s e-fuels webinar presented in collaboration with the National Renewable Energy Laboratory.