Towards the end of 2025, news coverage began to focus on affordability, and the price of new vehicles became a central proof point in articles of concern. The Transportation Energy Institute recognizes that affordability is a primary factor that should drive strategic development for the transportation sector, because if the consumer cannot afford or refuses to pay for a new market option, that option will fail. The news coverage was not wrong – and when we look at the data, there appears to be significant cause for concern.

Vehicle Prices

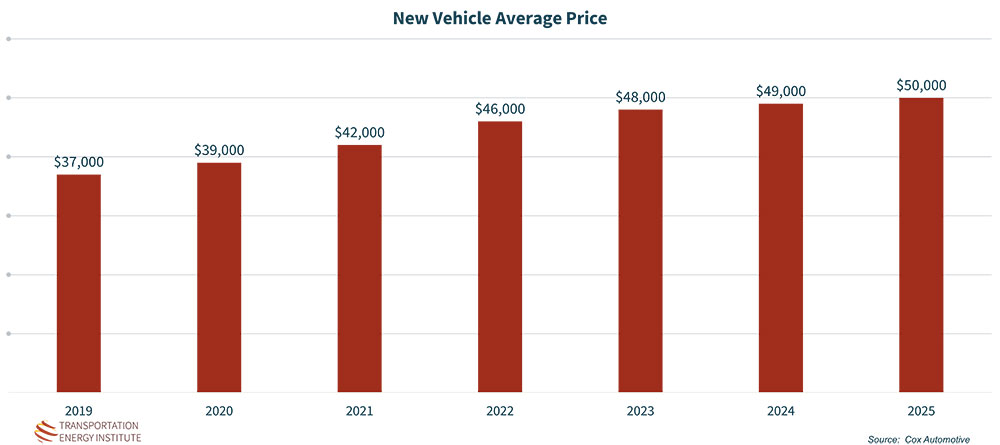

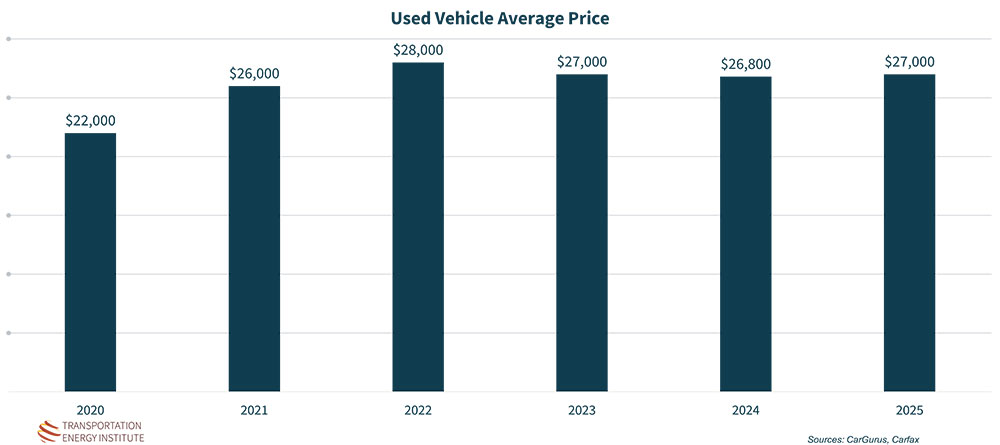

The most significant factor affecting the cost of vehicle ownership is the price of the vehicle itself. Between 2019 and 2022, the automotive industry faced historic inventory shortages due to the global semiconductor chip shortage and other pandemic-related supply chain issues. As demand far outpaced supply, prices soared. While inventory began to recover in 2023, prices did not return to pre-pandemic levels; instead, they remained at a new, higher baseline. By 2025, the average price of a new vehicle was above $50,000 and a used vehicle was above $27,000.

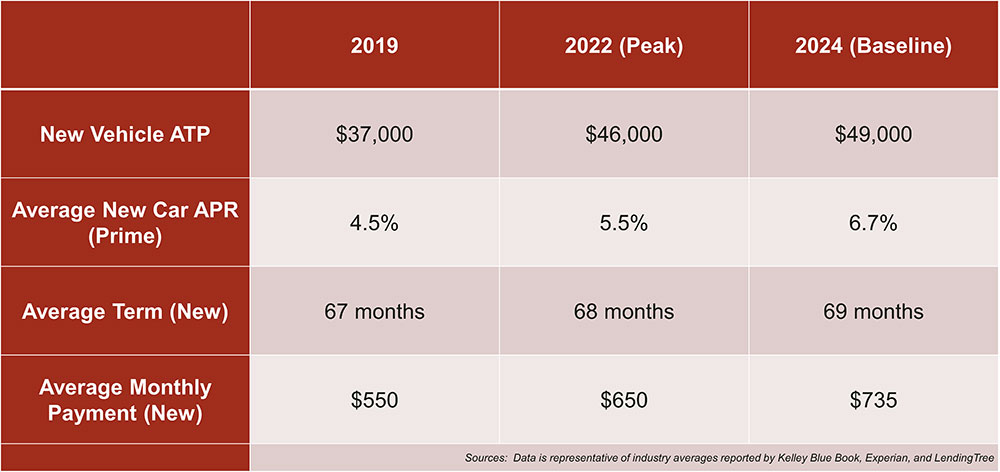

To keep monthly payments manageable in the face of these higher prices, consumers have been taking out much more expensive loans. By late 2025, according to Lending Tree, the average new car loan term was 69.1 months and 67.2 months for used cars. Some nonprime borrowers averaged terms as long as 75 months.

Meanwhile, interest rates for new and used cars, which had been relatively low, more than doubled. According to NerdWallet.com, average prime rates for new cars rose from approximately 4% – 5% in 2019 to 6.73% by early 2025. For used cars, the average rate climbed to 11.87%. For sub-prime borrowers, rates were much higher with new car loans as high as 15.81% for new and 21.58% for used vehicles.

The higher price of vehicles and higher interest rates, even with longer terms, resulted in higher monthly payments. According to Experian, average monthly payments by Q3 2025 reached $748 for new vehicles and $532 for used vehicles.

New Vehicle Cost Indicators (2019–2024)

Affordability

Between 2019 and 2025, the average new vehicle transaction price rose by 35%. In comparison, U.S. real median household income (adjusted for inflation) was flat. In 2024, the real median household income was $83,730, which was basically the same as in 2019 ($83,260).

Consequently, auto loan payments are taking a greater share of consumer budgets, putting significant stress on finances. While income was stagnant, the higher prices for new vehicles represented a significantly larger percentage of a household’s annual budget. A monthly payment of $748 on a new vehicle represents more than 11% of the total median monthly household income of approximately $6,800.

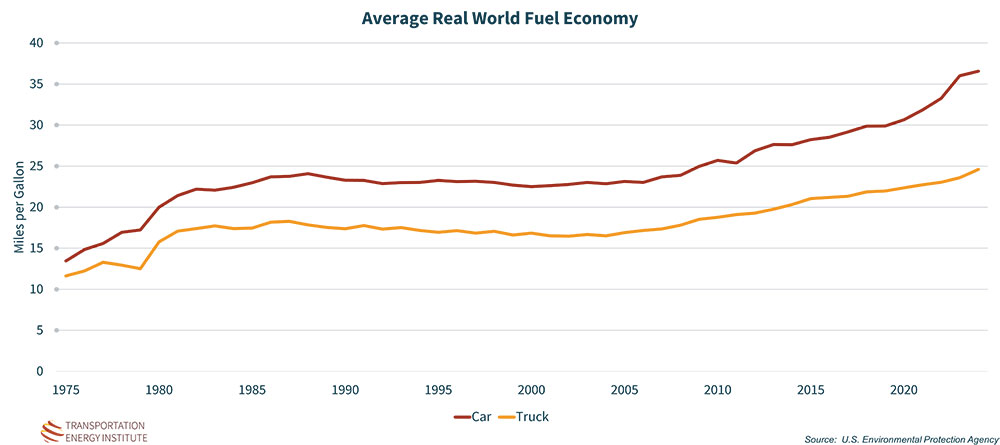

On a positive note, the fuel efficiency of the U.S. vehicle fleet continues to set records. In model year 2024, the average new vehicle achieved a record high of 27.2 MPG – 36.6 for cars and 24.6 for trucks. Despite consumer preference for heavier utility vehicles and trucks, technological advancements have continued to push efficiency upward.

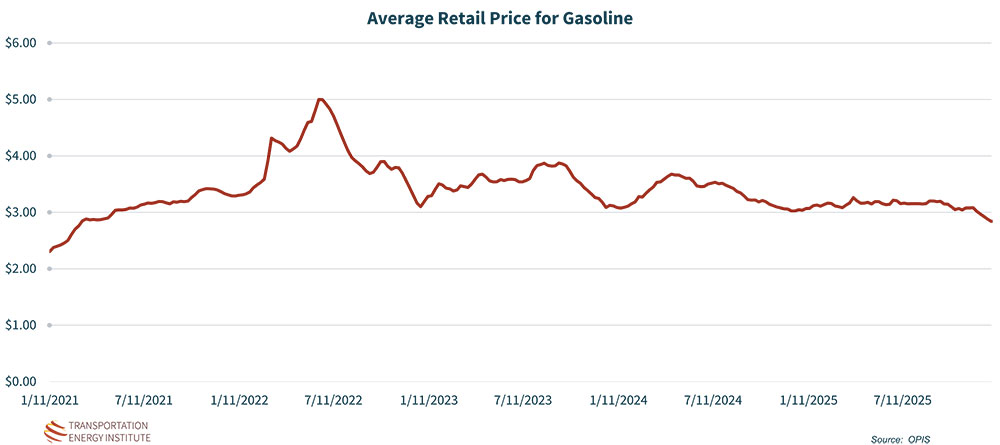

U.S. gasoline prices have been on a roller coaster, with the pandemic driving prices down and then geopolitical unrest driving them back up. Since 2021, prices averaged $3.40 on a weekly national basis, posting a low national average weekly price of $2.31 in January 2021 and a high of $5.00 in June 2022. The combined impact of fuel efficiency improvements and retail fuel prices have an effect on household finances. In 2019, consumers spent about $1,467 to drive 14,000. This increased to $2,105 in 2022 and dropped back down to $1,605 in 2025.

Variable Operating Costs (2019–2025)

Conclusion

With the increase in vehicle prices significantly outpacing the growth of household income, the burden of personally owned vehicles has increased. For many American families, car ownership has transitioned from a straightforward utility to a complex, long-term financial strategy that requires stretching debt across nearly seven years and leaving less monthly disposable income for other necessities.

For those thinking about the future of the transportation sector, it is essential to understand the economic impact of transportation on consumers as we consider strategies for reducing the environment impact of travel. Regardless how attractive a new option might be, a majority of consumers will likely be skeptical and resistant to embrace anything new unless it delivers a compelling price or quality of life advantage.