John Eichberger |

July 2024

Watching the Stanley Cup playoffs this year, I was surprised so many rinks and fans were using Bon Jovi’s “Livin’ on a Prayer” for motivation, singing “whoa, we’re halfway there,” as if they were halfway to the Cup. For most of them, they were “livin’ on a prayer” as only one team can win. (This year, it was the wrong team but let’s not quibble.) But as I reflected on the sentiment, I realized that the June 2024 vehicle sales data is available and that means we are halfway through 2024 and this is always a good time to see where things stand today. So, let’s take a look at which vehicles are selling and how they are trending.

According to WardsIntelligence, sales through June and entering into July have resulted in a seasonally adjusted annual rate (SAAR) projection of light duty vehicles (LDV) sales for 2024 of 16.1 million units. If this holds true and sales do eclipse 16 million units this year, that will be the first time that threshold has been crossed since before the pandemic. The SAAR is calculated each month to give an idea of where the market is heading. How accurate might it be? Well, since 2020, there have been 55 monthly SAARs calculated and 22 of those have predicted more than 16 million units sold. That said, the SAAR changes every month to factor in new developments in the market and seasonal factors that affect sales. If accurate, however, the vehicle industry is poised for a good year.

Powertrain Diversification

As we always do, we track the sales of vehicles with different powertrains. Through June, vehicles equipped with only internal combustion engines (ICE) remained dominant at 81.4%, although this continued a consistent decline in market share that began after 2016 when they commanded 97.2% of the market. Hybrid electric vehicles (HEV) remain the second most popular powertrain, jumping from 7.6% of sales in 2023 to 9.5% through the first half of 2024.This continued a growth trajectory that has seen market share increase from just 3.1% in 2020. Pure battery electric vehicles (BEV) remained at 7.1% share of the market, just below their 2023 average of 7.2%, but still up from 1.6% in 2020. Meanwhile, plug-in hybrid electric vehicles (PHEV) gained some share, climbing from 1.9% of the market in 2023 to 2.0% through June and up from just 0.4% in 2020.

Top 15 Vehicles

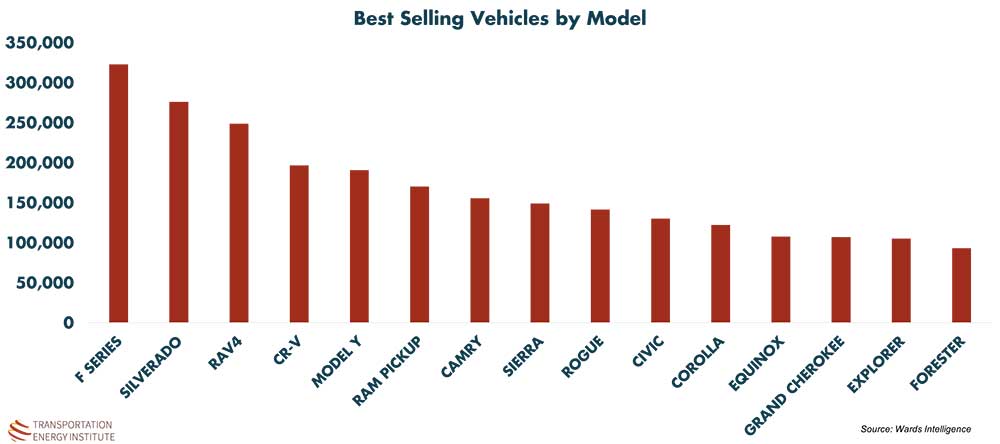

Again using WardsIntelligence data, the top 15 vehicles sold through June are not very surprising. Wards’ original listing includes all vehicles within a specific model and is presented below. The Ford F-series remains the dominant vehicle in the market (297,335 ICE, 33,674 HEV, 15,645 BEV), followed by the Chevy Silverado and then the Toyota RAV-4 and Honda CR-V. The Tesla Model Y commands the fifth position, a significant development for an all-electric vehicle to rank so high. The top six is rounded out by the Ram pickup after which the first passenger car enters the list in the form of the Toyota Camry.

But when we sort the data and separate specific models by powertrain variants, we get a slightly different view of the market. That is also presented below. In this assessment, the Model Y rises to the third most popular model in the U.S. through the first six months. This is very impressive, especially considering it is flanked on both sides by ICE-powered pickup trucks. The Honda Civic ICE then takes over sixth position as the most popular passenger car. Notably, the RAV-4, which was the third most popular model when all powertrains were combined, is eighth overall with its hybrid powertrain.

Crossovers Still Dominate

In a trend that has been consistent for more than a decade, the category of cross-over utility vehicle (CUV) remains the favorite option for American buyers, increasing its dominance over the first six months of 2024 to 49.1% of all vehicles sold. This is a jump over last year at this time when CUVs captured 46.4% of the market. Not only did CUVs dominate in units sold, but manufacturers also made available for sale approximately 200 different models and variants, giving buyers the greatest selection of options from which to choose.

It is worth noting that when we evaluate the top 10 CUVs sold through June, the Tesla Model Y is the number one model, selling more than 190,000 units. Positions two and three were in a dead heat, separated by fewer than 500 units with the RAV-4 HEV coming up just short of second place. Rounding out the top five was another HEV, the Honda CR-V.

Summary

If the SAAR can be relied upon, 2024 could be a good year for vehicle manufacturers, but we will see how the final six months play out. You never know what might happen in an election year.

When we look at sales data, it is important to look beyond the top line results. Those results tell us that ICEV remain dominant, hybrids continue to gain share and BEVs have steadied around the 7% market share threshold. However, diving a bit deeper uncovers some nuances that show that not all can be summed up in top line data. Certain models of BEVs and HEVs are performing very well and outpacing their ICE variants, which might indicate additional life for electrified powertrains assuming they are offered in vehicle models that consumers want.

And that is the ultimate message data has been telling us for years – consumers will buy the vehicle they want. If manufacturers want them to purchase alternative powertrains, they need to focus on delivering a vehicle the consumer wants – period. Otherwise, it doesn’t really matter what powertrain is being promoted. Remember, Tommy and Gina got each other and are gonna do what’s right for them – we gotta give them what they want.