September 8, 2020

The COVID economic shut down had a significant impact on all industries, but especially the vehicle market. Since everything began, stories have focused on the long-term impact for new vehicles sales and the devastation the shutdown wreaked on the market. Yet, some customers continued to purchase new vehicles and once the country began to reopen, the market seemed to bounce back (in terms of units sold) with some segments surpassing their 2019 performance. Which vehicles did customers purchase that helped accelerate the sales recovery?

In looking at the data, I realized that the vehicles that lead the rebound were the ones we would expect – the tried and true that always stand up against the odds. Those vehicle types and specific models that customers go back to time and again – the old, reliable friends. And of course this got my foot tapping to the kings of the punk-ska genre, Rancid and their radio single Fall Back Down:

If I fall back down

You’re gonna help me back up again

If I fall back down

You’re gonna be my friend

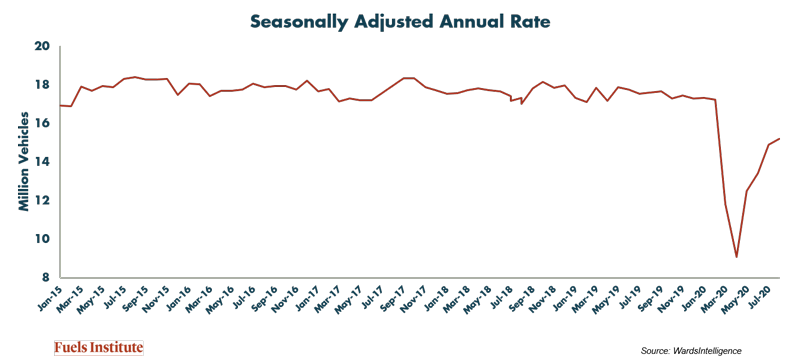

The industry uses a term called SAAR, which stands for Seasonally Adjusted Annual Rate, as a means of forecasting how many vehicles are expected to be sold in a given year. As the following chart demonstrates, the SAAR had been relatively steady in the 16 – 18 million unit range for the past several years – until COVID.

In April 2020, the SAAR dropped to 9.09 million – its lowest level since December 1981! (The lowest it reached during the Great Recession was 9.22 in February 2009.) The implications seemed devastating. Fortunately, the industry has rebounded quite a bit since April and in August the SAAR was back to 15.2 million. But again – what vehicles were people buying during the COVID pandemic?

Don’t worry about me I’m gonna make it alright

Got my enemies cross-haired and in my sight

I take a bitter situation gonna make it right

In the shadows of darkness I stand in the light

Ya see it’s our style to keep it true

I had a bad year, a lot I’ve gone through

I’ve been knocked out, beat down, black and blue

She’s not the one coming back for you

She’s not the one coming back for you

Resilient Technologies

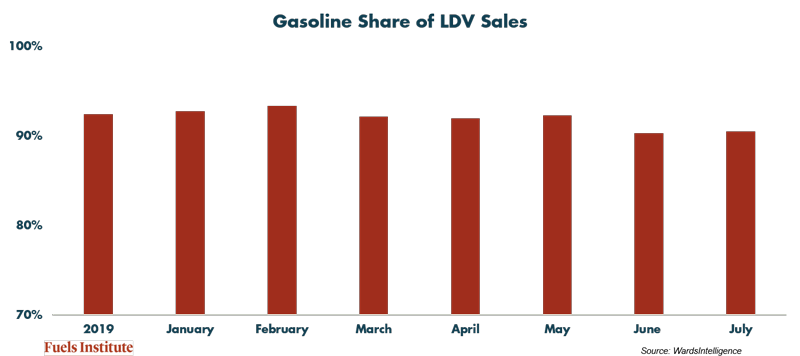

It should be no surprise that gasoline-powered vehicles continued to dominate during the pandemic as they have forever, maybe due to their sheer dominance in terms of vehicle availability. But when we pull gasoline out of the mix and look at the market share of different powertrains, some of the results are very interesting.

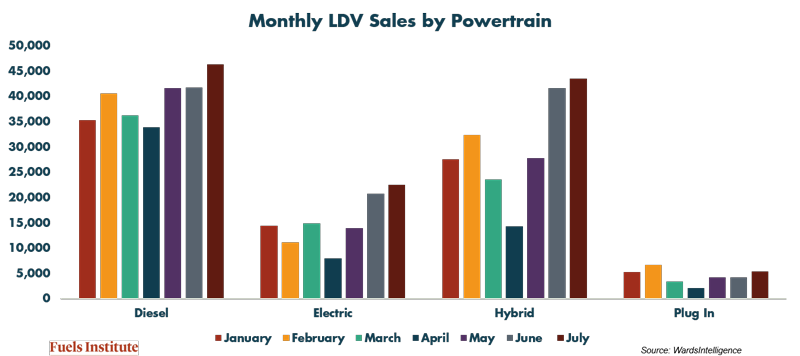

Diesel emerged as a strong option throughout the pandemic, increasing its share of total light duty vehicles sold from 3.3% in 2019 to 4.7% in April. In terms of total units sold, April sales only fell slightly below January numbers. This could show some resilience in the technology as diesel-customers continued to make purchases during the shutdown.

In the electrified market, there was quite a drop in sales in April, but the recovery was pretty quick, especially among hybrids where June and July sales significantly outpaced January sales. I am not sure what prompted this surge, but the jump in monthly sales as the country began to reopen should not be ignored. Meanwhile, sales of battery electric vehicles in June and July surpassed their 2019 market share indicating continued growth in interest in BEVs, despite the influence of COVID, as well as the availability of more options. I don’t think this indicates a change in consumer behavior due to COVID, but rather a return to evolving consumer preference that has been developing the past several years. Now that consumers have more options available within the electrified space, sales should continue to increase.

Customers Remain Committed to Vehicle Type

In July 2018, the Transportation Energy Institute published a report (“Driving Vehicle Sales – Utility, Affordability and Efficiency”) in which we presented data showing that consumers’ number one factor in selecting a vehicle was one that would satisfy their primary need. Our point was that a family of five will not purchase a compact, high-efficiency model as their primary vehicle because it does not satisfy their needs. Likewise, someone who needs a commuter vehicle that delivers great fuel efficiency is unlikely to purchase a large pickup truck. The “needs first” theory seems to continue running unabated, even during the panic of a pandemic.

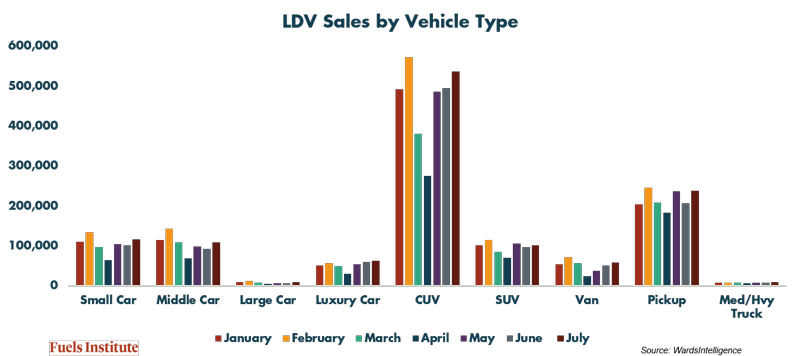

Crossover utility vehicles (CUVs) have emerged as the dominate vehicle category for more than the past decade and that is not changing anytime soon. And because they are the largest category, they also recorded the biggest drop in total sales in April. Yet, despite this slip they continued to leave all others in their dust in terms of market share.

One segment that seemed to benefit relative to others from the COVID-shutdown were pickup trucks. Overall, unit sales of trucks did not drop too much during the shutdown, but they represented a much greater percent of overall sales. In 2019, pickups represented 17.8% of LDV sales; this share jumped to 25.2% in April. It is clear that the pickup customer remained relatively undeterred during the pandemic, leading to several stories about the resiliency of the pickup truck, the love affair Americans have with their trucks and the impact on available inventories of this popular vehicle as sales continued but production ground to a halt.

So…Who Won?

I am not saying that vehicle sales are a game – but there is intense competition for the customer, so the question remains valid. From the basic data, it is clear that gasoline retained its crown, diesel showed its power, and hybrids rose from the shutdown and beat their 2019 numbers easily. Meanwhile, CUVs just smiled and kept on “truckin’” while pickups demonstrated incredible resiliency, filling a need that did not slow down. So that’s all great, but what about individual models?

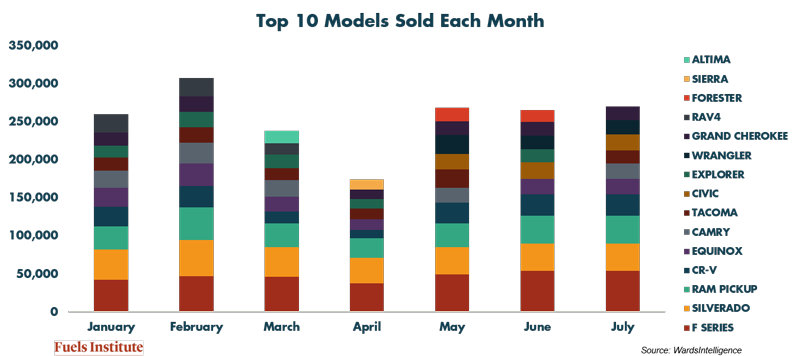

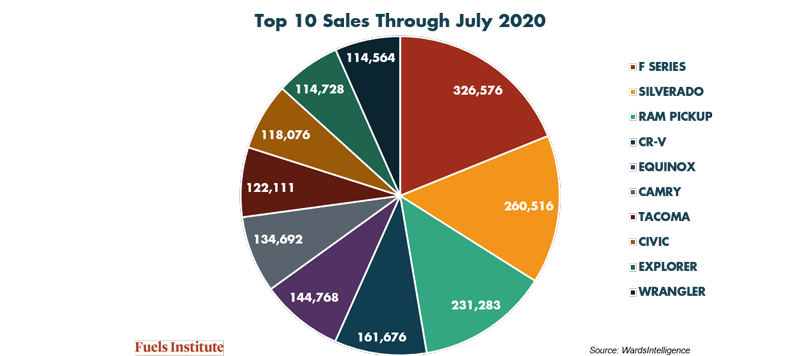

On a monthly basis, the top ten vehicles sold changed frequently. In fact, through July, 15 different vehicles occupied the top 10 sold list in a given month and only four were represented each month – F Series, Silverado, Ram and CR-V (the theme of pickups and CUVs continues).

Through the first seven months of 2020, however, the cast of characters representing the top 10 best-selling models was fairly predictable if you have been paying any attention to the market the past decade or so.

What’s Next?

It is clear from the data, that despite the interruption of the COVID shutdown, the light duty vehicle market was able to hop on the back of historically strong performers and popular vehicle types to pull itself up by its bootstraps and charge into the second half of the year with some momentum.

How 2020 ends remains to be seen, but it appears that despite the pain of the pandemic mitigation measures implemented this past spring, the light duty vehicle market will emerge looking quite similar to how it ended 2019. It makes me wonder what it will take to prompt consumers to change their behavior and begin to purchase different vehicles? The pandemic clearly did not do it – I guess we will have to wait and see.

It takes disaster to learn a lesson

We’re gonna make it through the darkest nights

Some people betray one and cause treason

We’re going to make everything alright…whoo!