February 24, 2022

The price of oil and gasoline is once again dominating news coverage, and with good reason – prices haven’t been this high since 2014. With such coverage comes a lot of political debate, from those blaming politicians for the increase in prices (fyi, the President does not control prices) to politicians proposing “solutions” to reduce the prices being paid by their constituents. Proposals ranging from a federal gas tax holiday to releasing oil from the Strategic Petroleum Reserve are temporary initiatives that might sound appealing at first glance, but do not impact the long-term fundamentals that have contributed to elevated prices. The bottom line to understanding prices has its roots back in high school economics – supply and demand. In an effort to move away from the rhetoric, let’s take a look at some historic data that will provide insight into some of the fundamentals affecting the market today.

Before we begin, let me point out that we wrote about the impact of the pandemic on the oil and gasoline markets in October 2021, and those elements are still contributing significantly to conditions today. I encourage you to check out that article as well as we won’t be rehashing those points exhaustively in this article.

What makes up the retail price of gasoline?

For the past 20-plus years, I have been called upon to explain why gasoline prices go up and down and what causes this volatility. Consequently, since January 2006 I have been tracking relevant data on a weekly and monthly basis. Therefore, most of the historic data I present in this article reaches back 16 years – which is a pretty good benchmark and incorporates some major disruptive events to help explain how external factors can affect the market.

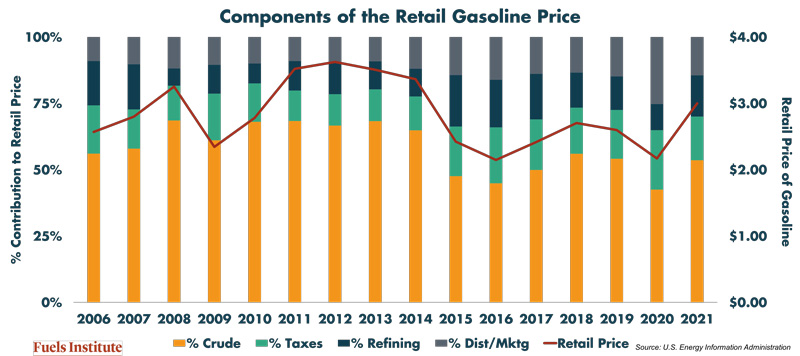

The number one factor that influences retail fuel prices is the price of crude oil. Each month, the U.S. Energy Information Administration (EIA) posts a dissection of the retail price of gasoline and diesel fuel, breaking them down into four component parts – crude oil, taxes, refining and distribution/marketing. Let’s take a look at each individually:

- Crude Oil – Since 2006, on average crude oil has been responsible for 58% of the retail price of gasoline. This contribution has ranged from a high of 80% in December 2011 to a low of 25% in April 2020 (this was when crude oil traded for a negative price during the most extreme conditions of the COVID shutdowns). As of December 2021, it was right near its average of 53%.

- Taxes – Typically the second largest component, taxes contribute on average 16% and have ranged from a high of 26% in April 2020 to a low of 10% in July 2008. Taxes are typically a set on a per gallon basis and do not fluctuate much throughout the year, so their contribution is relative to the more volatile values of other components. The federal excise tax adds 18.4 cents per gallon, but state assessed taxes can range dramatically from a high of an additional 68 cents in California to a low of 15 cents in Alaska. A list of state taxes is available from API.

- Refining – The costs to convert crude oil into a product that vehicles can use in their engines contributes on average 13% to the price at the pump. This has ranged from a high of 28% in April 2007 to a low of -4% in November 2008.

- Distribution and Marketing – This category includes everything that happens after the refinery converts crude oil into gasoline, including pipeline transport, terminal operations, wholesale distribution and retail operations and profits. On average, it contributes 13% to the pump price and has ranged from a high of 46% in April 2020 to a low of -4% in May 2009.

Where have prices been?

Crude oil prices, which are traded on several commodities markets, can be quite volatile and are influenced heavily by actual supply and demand conditions, projected changes in production and economic activity, current and anticipated geopolitics and speculation about what policies and actions governments might take. It is a very challenging market to understand because it is influenced by so many variables. There are two primary crude oil benchmarks, West Texas Intermediate Crude and Brent Crude. After setting record lows in April 2020, both benchmarks began their price recovery later that summer and by December 2021 exceeded their 16-year average. As of the first week of February they were 26% and 23% above their averages, respectively.

Retail gasoline prices hit their recent low price point in May 2020 and began their sustained recovery in November of that same year. Prices matched their historic average in March 2021 and by the beginning of February 2022 were 22% above their average.

How do crude oil prices relate to retail gasoline prices?

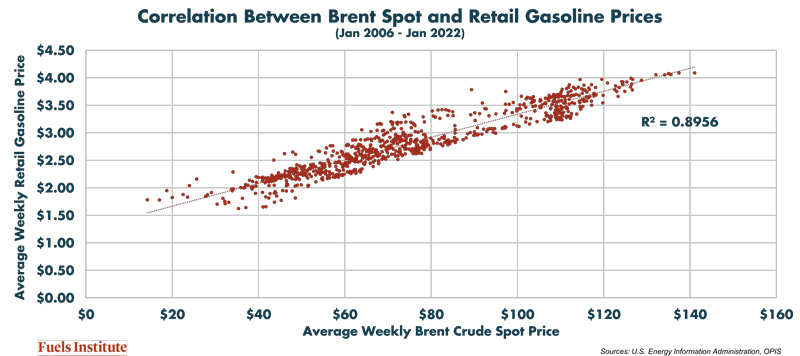

To best understand the relationship between crude oil and retail gasoline prices, it is helpful to look at the correlation between the two. A correlation coefficient of 1 or -1 indicates the two variables are perfectly correlated. When we compare the global benchmark Brent crude oil spot prices with retail gasoline, the correlation is almost perfectly linear at 0.89. This means that when crude oil prices increase, it is pretty predictable that retail pump prices will follow suit.

Do gas prices influence demand?

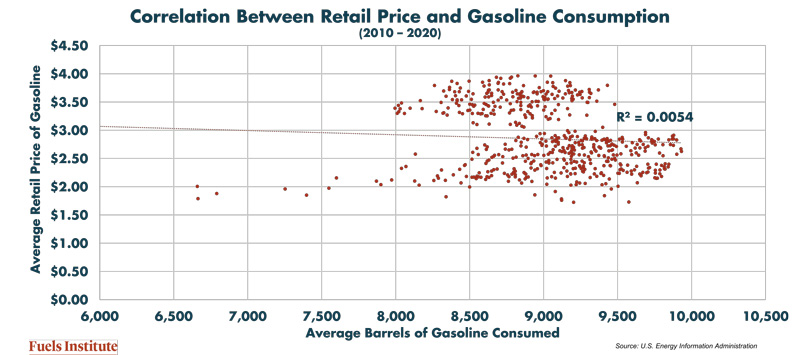

By contrast, higher pump prices do not necessarily result in reduced demand. So often, headlines will assert that high prices at the pump have inspired significant change in consumer behavior by reducing travel, carpooling or purchasing fuel efficient vehicles. The reality is quite different.

The Transportation Energy Institute published a report in 2018 that analyzed 15 years of vehicle sales data and concluded that the primary influential factor in determining what vehicles consumers purchase is centered around their needs – they seek vehicles that satisfy the needs of their household. For example, a family of five is not going to purchase a subcompact regardless of pump prices. Vehicle cost and efficiency are also critical factors, but only within the class of vehicle they have selected.

In addition, we have evaluated several data sets relative to retail prices and fuel consumption and have found virtually no statistical correlation between the two. In general, we can assume that consumers are going to drive when and to where they need to drive regardless of pump prices. The data below is drawn from EIA published data on prices and consumption from 2010 – 2020. The correlation coefficient is almost 0, indicating no linear relationship. We also have evaluated other data sets from 2,000 retail stations over a 12-month period and found similar results. Basically, higher prices historically have not materially changed consumer driving behavior.

Do gas prices affect other aspects of the economy?

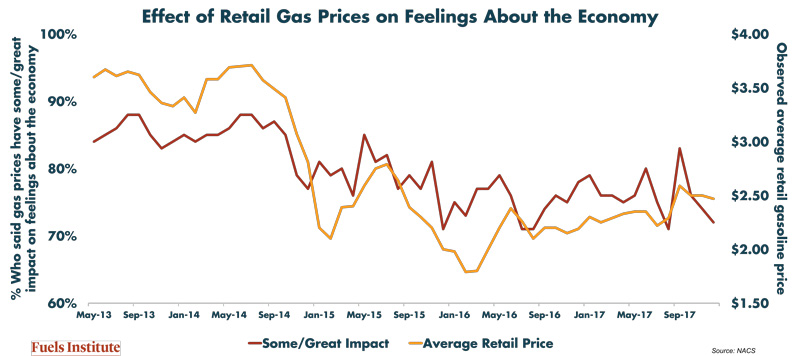

This does not mean consumers are ambivalent to pump prices. We know from experience that increasing prices on the corner sign have a significant effect on consumers, especially with regards to how often fuel prices are a topic of their daily conversations, which is directly related to the amount of media coverage. Gasoline price signs are prominent in their daily routine and serve as a bellwether about the economy in general. Over five years, NACS surveyed consumers monthly to understand the influence fuel prices might have on their behavior and their feelings about the economy. That project found consistently that 80% of consumers said the retail price of gasoline has some or a great impact on their feelings about the economy, although the influence does wane when prices are retreating. So, while gallons consumed may not fluctuate much with an increase in price, other economic indicators may demonstrate a more significant reaction.

Are today’s prices out of step with historic averages?

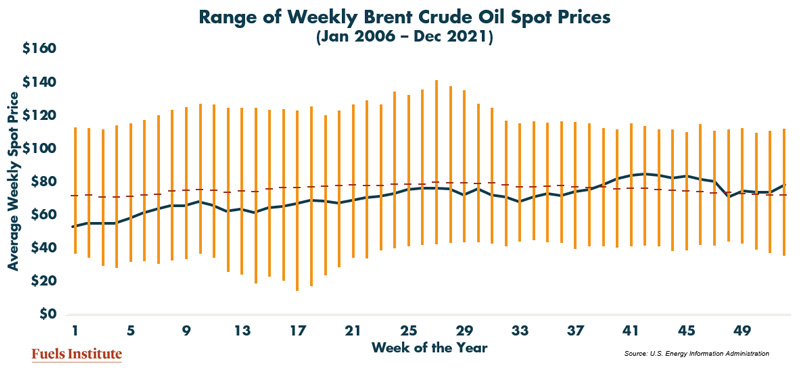

If we look at the range of prices by week since 2006, we observe significant variability with a relatively consistent average throughout the year. The blue line in the following charts is the weekly Brent crude spot price and retail gasoline price for 2021 and is presented as a basis for comparing recent conditions with historic averages. Crude oil was still relatively consistent with its historic average until the end of the year but remained far below its historic peak in any given week. Conversely, retail gasoline prices floated above their historic average for most of the year before diverging more significantly near the end, at which point they consistently matched their historic peaks in the final weeks of 2021.

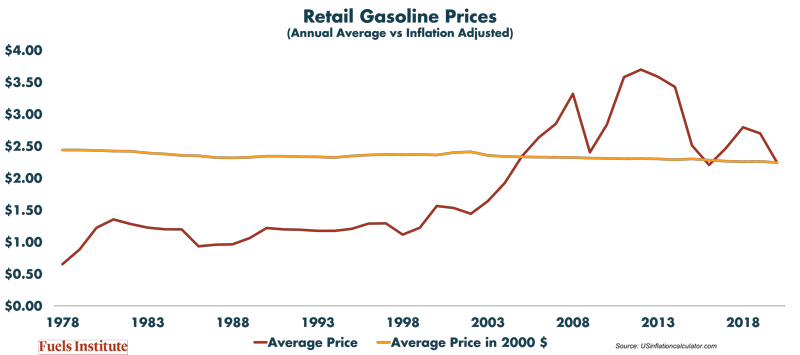

Gasoline prices have been relatively stable since the late 1970s when adjusted for inflation. As the following chart shows, in constant 2000 dollars the price of gasoline has $2.34 per gallon, with a variability that ranges from $2.24 to $2.44. While the posted price may send shockwaves through society, the affordability of gasoline has not changed much in more than 40 years.

What can we expect looking forward?

We have all been cautioned by financial advisors that historic performance is not an indicator of future performance, and this is true for the fuels markets as well. However, there are lessons we can learn from the past. Sharp changes in crude and retail fuel prices over the past 16 years can be attributed to significant changes in supply and/or demand.

- 2008 – Buoyed by strong economic performance, crude oil prices set a record of morel than $140 per barrel, and then the world entered the Great Recession and prices dropped 75% in five months. This was followed by a protracted recovery with prices not recovering to their 16-year average until 2011.

- 2014 – Strong global oil supplies, driven by domestic production in the U.S. and increased production by OPEC, came into sharp contrast with significant economic slowdowns in China and Europe, sending crude prices down more than 50% in four months. The market recovered slowly to match its historic average in early 2019.

- 2019 – COVID-19 sent the world spinning and the bottom once again fell out of the market. Economic shutdowns decimated energy markets and economies in general, resulting in oil trading at a negative value for the first time in history.

- 2021 – As the world emerges from COVID and economies ramp back up, the loss of production capacity in the aftermath of the pandemic and an increased aversion to economic risk with regards to significantly increasing production is contributing to an imbalance in supply and demand. Add to this significant uncertainty regarding the pace of recovery post-pandemic and the geopolitical risks associated with the war in Ukraine, commodities traders are nervous about what the immediate future holds and had already incorporated risk into the price of oil prior to the Russian invasion.

Ultimately, there are no short-term fixes to drive down prices – only sustained stability and a rebalancing of supply and demand will provide relief at the pump. When this will occur is anyone’s guess.