July 9, 2020

Lost among the excitement and hype associated with vehicle electrification is the fact that 98% of vehicles sold in the U.S. in 2019 were liquid fueled. Further, according to the U.S. Energy Information Administration (EIA), at the beginning of 2020, 99.2% of the 258.6 million light duty vehicles (LDV) in the United States were powered by liquid fuel. Even though electric-drive vehicles are the up and comer technology and will play a significant role in the market in the near future, when we consider that the overwhelming majority of drivers continue to rely upon liquid forms of energy, it seems the attention paid to electricity is disproportionate. The two will co-exist for decades and we cannot ignore this incredible market just because something shiny and exciting is on the horizon – the tried and true of the past 100-plus years will be around.

Thanks to a recommendation of my colleague, we are reaching back to 1973 and pulling from the great classics of Motown with the Spinners, “I’ll Be Around.” I think it is appropriate for this edition of “The Commute,” because as we look at the data and recognize that many have become enamored with electric vehicles (including many manufacturers), the internal combustion engine and liquid fuels will still be around – for a long time, although they will evolve.

This, is our fork in the road

Love’s last episode

There’s nowhere to go, oh no

You made your choice, now it’s up to me

To bow out gracefully

Though you hold the key, but baby

Whenever you call me, I’ll be there

Whenever you want me, I’ll be there

Whenever you need me, I’ll be there

I’ll be around

With that said, what is going on in the liquid fuels market? In a word: plenty.

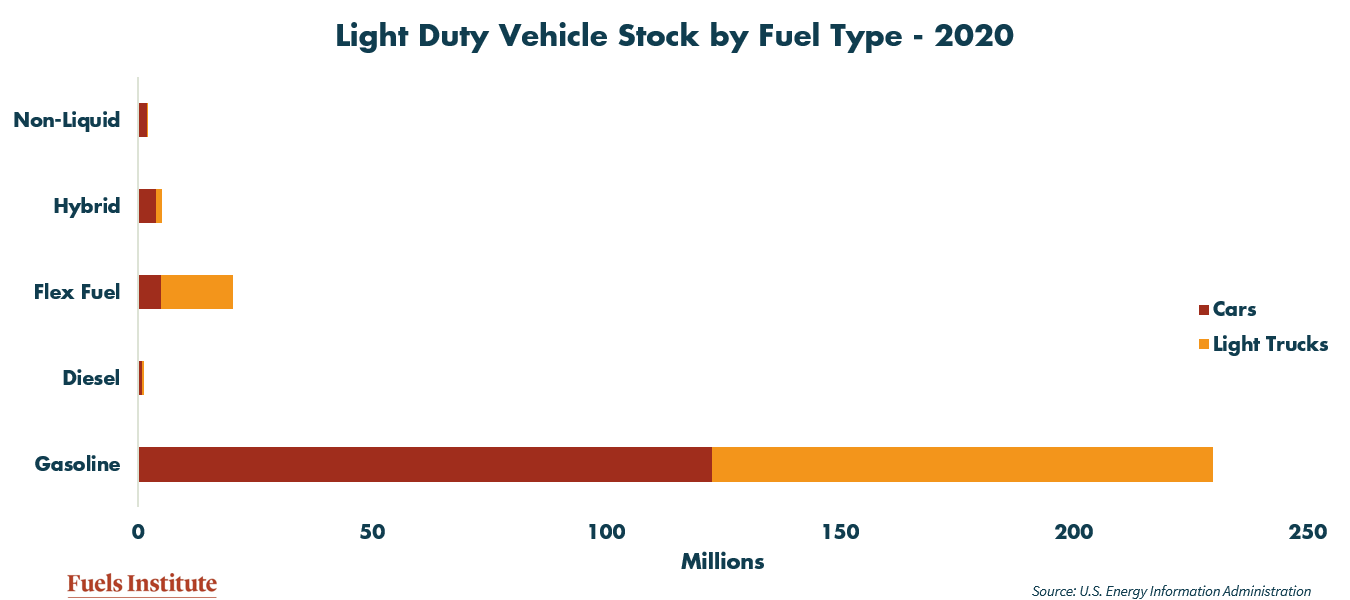

U.S. Light Duty Vehicle Fleet

When thinking about the transportation energy market, it is important to think about the composition of the existing fleet. At the beginning of 2020, gasoline light duty vehicles comprised 88.9% of all vehicles. Flex fuel vehicles (FFVs), capable of running on straight gasoline or a mixture of up to 85% ethanol, were the second most populous vehicles at 7.8%. Diesel and hybrids represented 0.5% and 1.9%, respectively. (Included in the definition of liquid fuels for this article are traditional hybrid electric vehicles, or HEVs, which require gasoline to operate and use their battery to supplement the internal combustion engine.)

Diversifying the Gasoline Market

The gasoline segment can be a little misleading if one assumes that these vehicles run on pure gasoline. As most readers know, the vast majority of gasoline in the United States is blended with 10% ethanol, which contributes to the fuel’s octane and enables refiners to comply with the federal Renewable Fuel Standard.

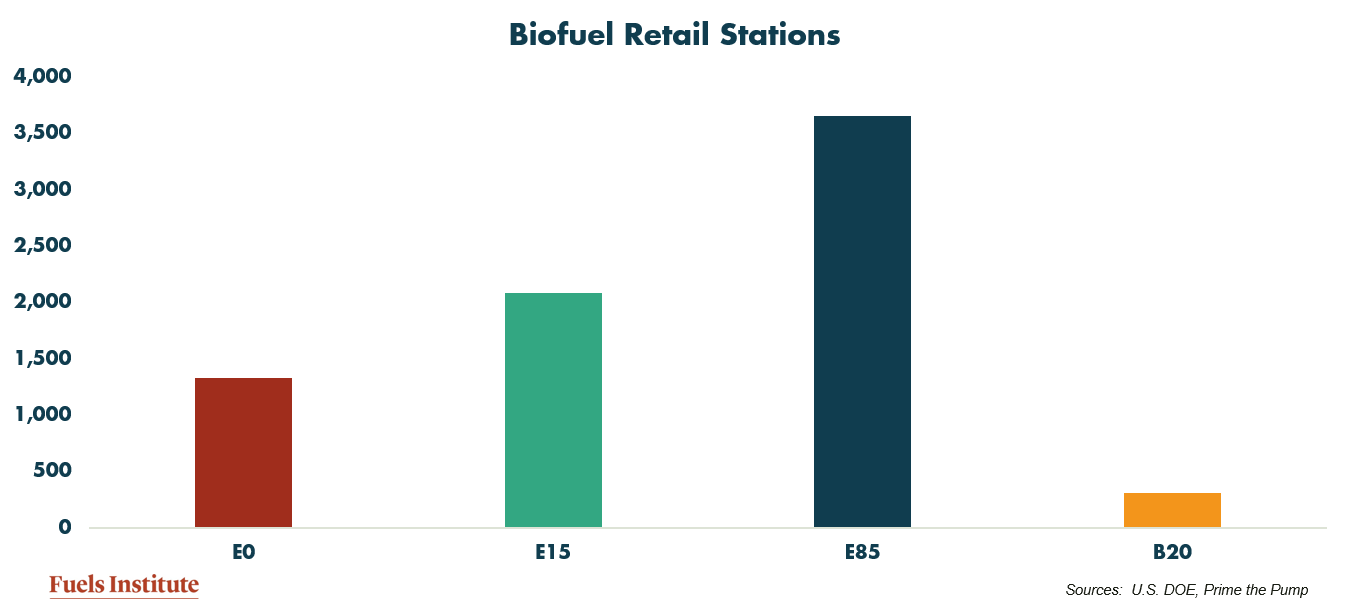

In recent years, however, there has been further diversification within the gasoline pool with retailers opting to sell gasoline containing up to 15% ethanol and delivering slightly higher octane (88) than regular unleaded (87), usually at a more attractive price. This fuel, known as E15, is sometimes sold as Unleaded 88 or some other name and is approved for use in on-road vehicles manufactured since 2001. According to the organization Prime the Pump, at the beginning of the year there were approximately 2,100 retail stations selling E15.

Contrary to the move towards offering gasoline with higher blends of ethanol, there has also been an increase in the number of stations selling ethanol-free gasoline. There are some consumers who do not wish to purchase gasoline containing ethanol, for a variety of reasons, and they are willing to pay a premium price for this type of fuel. According to the Oil Price Information Service, there are more than 1,300 stations in the U.S. selling E0, or clear gasoline.

And then there is the market for E85 that can only be used by specially adapted vehicles known as flex fuel vehicles (FFV). E85 is a mixture of gasoline with ethanol ranging from 51% – 83% by volume. For many years, vehicle manufacturers received a credit towards complying with the Corporate Average Fuel Economy (CAFE) standards for each FFV they manufactured. This credit expired in 2019 and has not been reinstated, although there are efforts being made to provide some sort of incentive to manufacturers to continue producing these vehicles. According to the Alternative Fuel Data Center provide by the U.S. Department of Energy, there were 3,652 public stations selling E85 in June 2020. However, Prime the Pump places the number at closer to 4,600 at the beginning of 2020. The discrepancy between these numbers has existed for years and could derive from what is considered a public station.

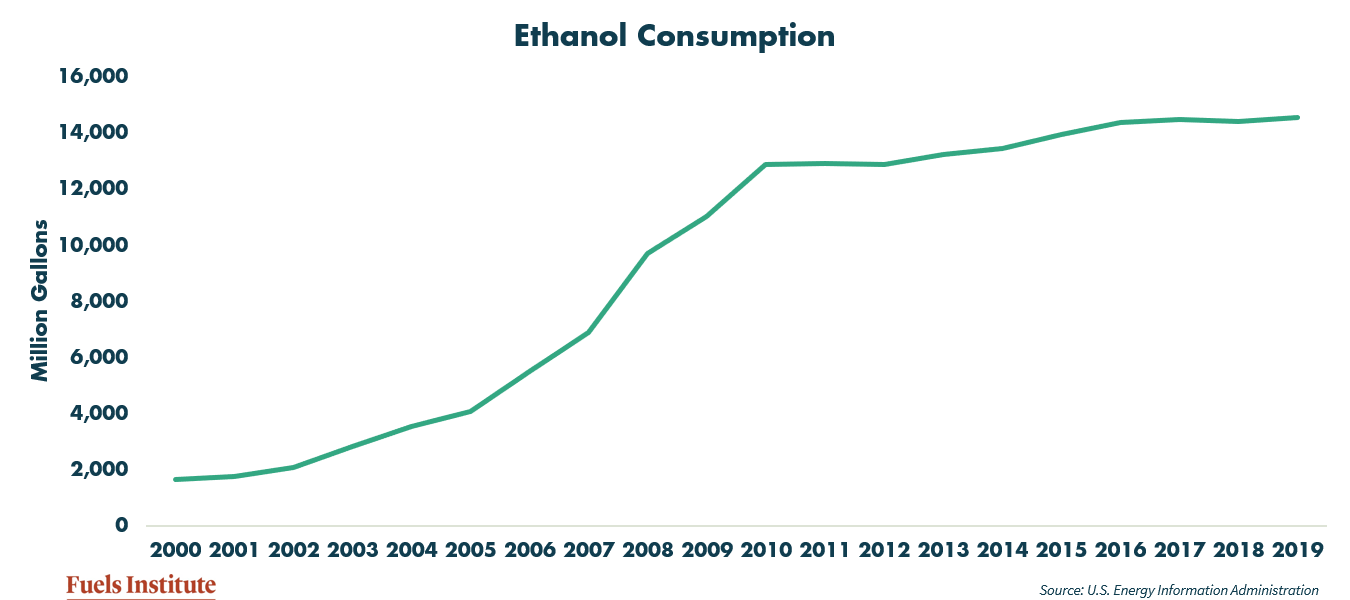

The policies and market forces influencing the liquid fuels market have resulted in a significant increase in the overall consumption of ethanol, with the Renewable Fuel Standard (RFS) having the greatest impact on the market. This is reflected in EIA’s report of ethanol consumption, which shows a tripling of consumption between 2005 and 2010. This period of growth was driven initially by the Energy Policy Act of 2005, which resulted in the rapid withdraw of the fuel additive MTBE from the market, creating an immediate increase in demand for ethanol within Reformulated Gasoline markets, and initiated the first RFS to take effect in 2007. Then, the Energy Independence and Security Act of 2007 amended the RFS to establish a goal of blending 36 billion gallons of qualified renewable fuels into the fuel supply by 2022. EISA also put a 15-billion-gallon limit on the amount of traditional (i.e., corn-derived) ethanol that could contribute to RFS compliance, the effect of which is shown in the data as ethanol consumption somewhat leveled off at just below 15 billion gallons beginning in 2016.

Diesel Fuel Diversification

Within the diesel segment, there is further diversification with blends of biodiesel and renewable diesel. Biodiesel is marketed at various levels, from relatively de minimis blend levels (5% or lower is considered by ASTM to be equivalent to diesel fuel and does not require additional labeling or disclosure) to B20 and some cases B100. Since blends up to B5 are not disclosed, the best way to quantify the volume consumed is to measure the volume of B100 produced and imported into the U.S, less any exported gallons of neat or blended biodiesel.

Biomass-based diesel is included in the 2007 RFS with a requirement originally set at not less than 1 billion gallons. The biodiesel requirement for 2020 and 2021 has been set at 2.43 billion gallons. Because biodiesel reduces greenhouse gas emissions by 50%, as compared to a gallon of diesel, biodiesel credits may be leveraged to meet other RFS fuel compliance demands. Today’s RFS biomass-based diesel renewable identification number (RIN credit) is currently $0.825/gallon. (What appears in this article is a very basic look at the biomass-based diesel market. For a more complete analysis of the market, please see the 2019 Transportation Energy Institute report, “Biomass-Based Diesel: A Market and Performance Analysis.”

The other major influencing factor is the blenders tax credit, which for years has teetered between in effect, expired and then retroactively reinstated. The inconsistency has plagued the biomass diesel market for years and it was not until 2020 that greater stability to secured. The tax credit ($1.00 per gallon of B100 and is exempt from income tax) is now authorized through 2022.

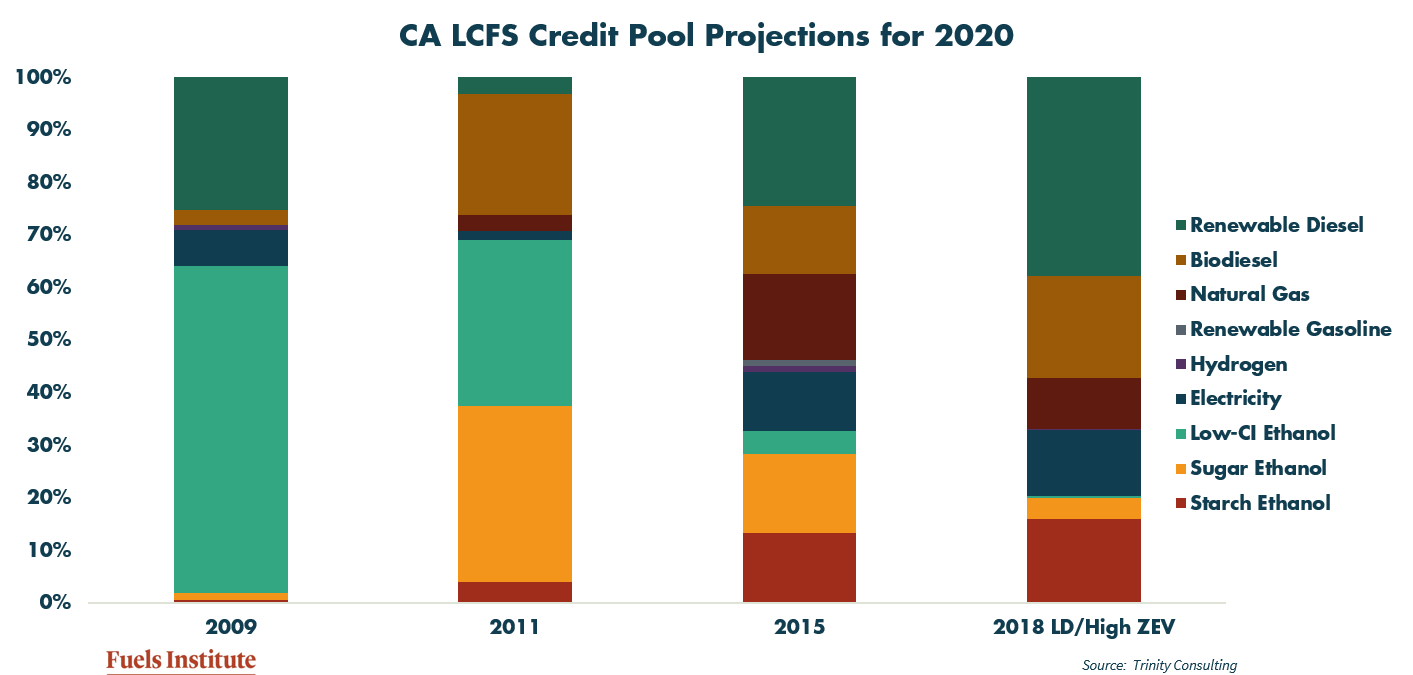

Another driving force for both biodiesel and renewable diesel consumption is the California Low Carbon Fuel Standard (LCFS), which provides a compliance credit on top of the federal blenders credit, making these fuel products very attractive economically. In 2018, California estimated that biomass-based diesel would generate more than 57% of required compliance credits. (For more details on the LCFS, please see the 2019 Transportation Energy Institute report, “Market Reactions to Low Carbon Fuel Standard Programs.”)

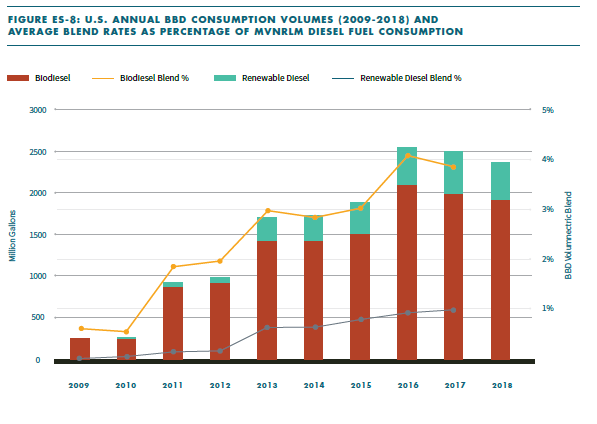

Data for renewable diesel, which is considered substantially similar to regular diesel fuel, requires no special handling requirements and can be used by all vehicles either blended with diesel or alone, is not presented as easily by the U.S. EIA as are ethanol and biodiesel. But, its value in terms of RFS and LCFS compliance, along with the blender’s tax credit and its compatibility with the existing infrastructure and vehicles (i.e., it is considered a “drop in” fuel), has given renewable diesel a significant boost in the past couple of years. The chart below is taken directly from the Transportation Energy Institute report on the fuel. From this data, it is clear that the past three years have been very good for expansion of the renewable diesel market.

Conclusion

The market for liquid fuels is strong and dominant and, even under the most aggressive but realistic forecasts, will continue to be critical to transportation for decades to come. But that does not mean the market is standing still and just waiting to be run over by a fleet of electrified vehicles. The fuel supply has diversified and continues to be evaluated for improvements. More stringent emissions regulations enacted by the government are clearly driving much of that, just as similar requirements are pushing the market towards electrification. But to think that anything not electrified is unimportant would be utter nonsense. We must be focused on all forms of transportation energy and must not overlook 99% of the market just because it does not fit into the story being crafted by many advocates, policymakers and the media.

The basic reality is this – internal combustion engines powered by liquid fuel will continue to move people from point A to point B and will do so alongside an increasing population of electrified vehicles. It is not an either/or situation. As Deion Sanders told Jerry Jones in 1995 Pizza Hut commercial: Football or baseball? Offense or defense? $15 or $20 million? It’s “Both.””

I’ll be skipping and jumping, I’ll be there

I’ll be a-rippin’ it up, I’ll be there

I’ll be calling out your name to let you know

I’ll be around