John Eichberger |

June 2026

When gasoline prices spike, consumers feel it instantly at the pump, prompting immediate shifts in weekend travel plans or discretionary household budgets. But when diesel prices increase, the impact on the entire economy can be much more significant. This is because nearly every item that consumers purchase and consume is delivered by a truck, and according to the Engine Technology Forum, 76% of the 17 million commercial vehicles in the U.S. run on diesel fuel. Consequently, when diesel prices go up the impact is felt by everyone – not just those buying the fuel.

Why have diesel prices increased?

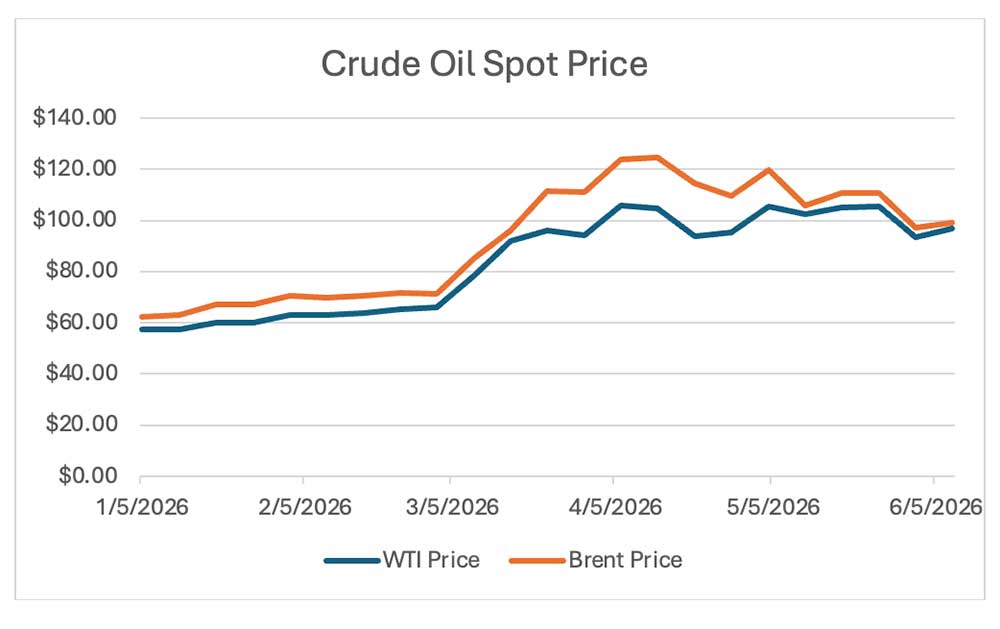

The conflict in the Persian Gulf has had a significant impact on the petroleum markets and most of the increased price in diesel fuel can be attributed to that situation. Since February, crude oil (which according to the U.S. Energy Information Administration is responsible for nearly half the retail price of diesel fuel) went up 67% from mid-February to mid-May. As could be expected, the wholesale price of diesel fuel increased 74% and the retail price increased 54%.

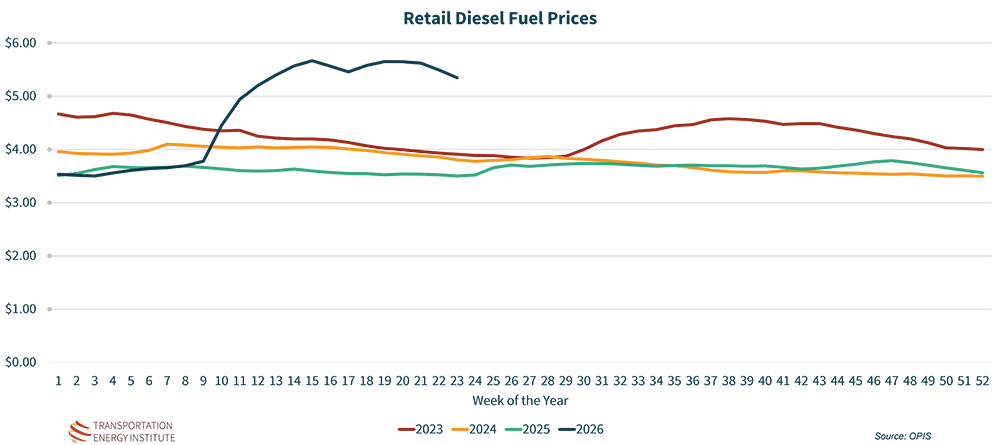

According to OPIS, the national average retail price of diesel fuel in May was $5.635 and ranged from a low of $4.66 in Oklahoma to a high of $7.21 in California during the first week of June. The May 2026 average compares with $3.546 in May 2025, $3.938 in May 2024 and $4.04 in May 2023. It also compares with $3.537 in January 2026. Clearly, the market is reacting to global events.

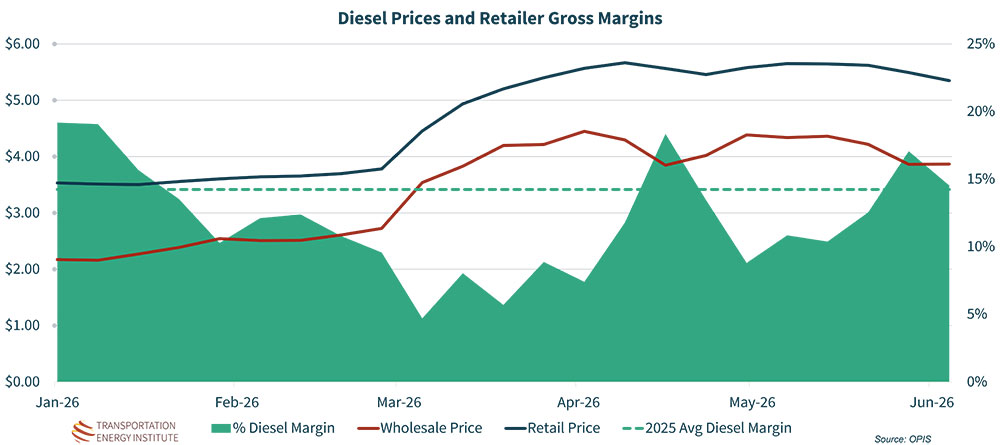

This relationship between wholesale and retail prices is typical – as crude oil and wholesale fuel costs increase, retail prices follow suit but usually at a slower pace. In fact, during the run-up in prices this year, retailer gross margins (the difference between posted retail prices and wholesale costs, not factoring in expenses) contracted and averaged 12% through mid-June compared with an average of 14% throughout 2025. Retailers typically lose margin when prices go up and recover as prices go back down.

What happens to the economy when diesel prices increase like they have this year?

Similar to fuel retailers, when prices increase transport companies see immediate margin contraction and, while they can utilize fuel surcharges to pass along costs, these are not implemented or adjusted immediately. Fleets often experience a one-week delay in adjusting surcharges based on changes in diesel prices, while railroads can face a 30-to-60-day structural lag in contract adjustments. When prices are going up rapidly, the effect on trucking operating expenses can be severe.

Once the surcharges catch up to fuel prices, the increased cost of moving goods from ports to distribution centers and ultimately to retail shelves means consumers pay higher prices for everyday retail items. A single product is often carried by several different diesel-powered vehicles before it reaches the customer. This includes moving raw ingredients to production facilities then on to the wholesale storage and distribution stage and ultimately final mile delivery. Operators at every stage of this system have to cover their fuel costs, resulting in compounded price pressure on the final retail product.

This pressure affects every element of the economy. Below are some major sectors worthy of note:

Food: Diesel is fundamental to the agricultural sector, powering everything from heavy farming equipment and tractors to irrigation pumps, utility vehicles, and other major equipment. When price increases occur at the same time as spring planting or fall harvest, farmers incur an immediate increase in operational expenses. These upfront costs, combined with subsequent transportation costs to move their products to processing plants and grocery aisles, create a compounding effect that drives food inflation higher while tightening margins for farmers.

Industry: Heavy industry and construction rely on diesel for material handling equipment, backup power generation, and moving dense, high-mass raw materials such as steel, concrete, and timber. High diesel costs act as a direct operational headwind, typically resulting in both depressed margins and project delays. As the cost of operations increases, builders and developers frequently slow down major infrastructure projects to limit exposure to peak prices and benefit from the following period of lower prices.

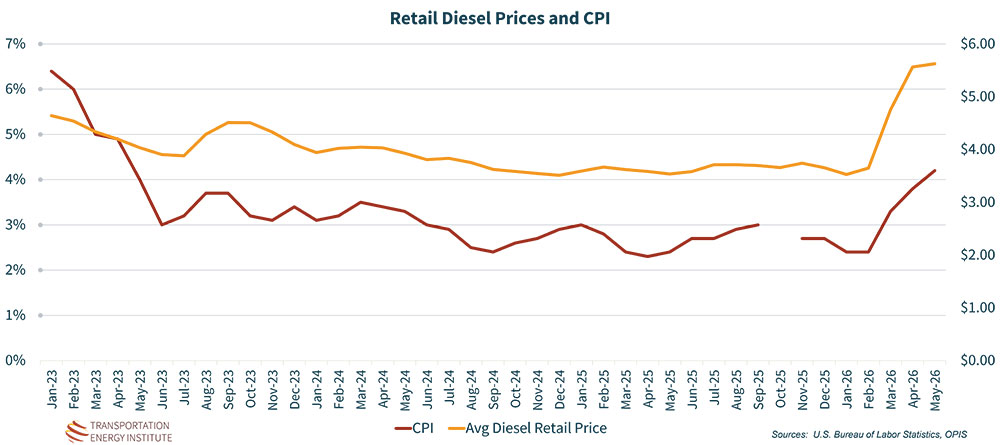

Inflation: Because fuel prices are highly visible, sustained increases have a significant impact on broader inflation metrics and consumer sentiment. Large and sudden increases in the Consumer Price Index (CPI) are often attributed to higher energy prices. This combined pressure on key economic indicators can lead the Federal Reserve to potentially hold interest rates higher for longer to cool demand. Unfortunately, this also increases borrowing costs for businesses trying to invest, refinance debt, or expand operations. An analysis of the monthly average diesel fuel price and monthly CPI since January 2023 yields a correlation coefficient of 0.63, which is considered a moderate to strong positive relationship.

Demand: When diesel and broader energy costs remain elevated for extended periods, they eventually affect overall demand. To reduce overall costs, freight movements may be slowed or reduced, shipments consolidated, routes optimized or non-essential transit suspended. As the pass-through of diesel costs hits essential items like food and household necessities, consumers are forced to reallocate their limited budgets away from discretionary spending (such as restaurants, entertainment, and non-essential retail), causing a secondary slowdown in the broader service sector.

Conclusion

Restoration of global flows is essential to bringing relief to the diesel market. At the time of this writing, there were reports of a potential deal to end the conflict in Iran and restore the functionality of the Strait of Hormuz. While such announcements typically are immediately reflected in the commodity price of oil and refined products, the restoration of supply will take significantly longer.

During a TEI-hosted webinar in mid-May, Debnil Chowdhury from S&P Global Energy and Denton Cinquegrana from OPIS made it clear that recovery to pre-conflict supply conditions could take up to 18 months. (TEI encourages interested readers to watch the webinar recording – it is filled with valuable insights from two of the most knowledgeable in the industry.) With the U.S. currently in the midst of its heaviest demand period of the year, the market may not react to changing geopolitical conditions as rapidly as will the futures market and the longer supply disruption persists, the more significant will be the impact on the general economy.